- March 19, 2025

- Posted by: Amit Pabari

- Category: Uncategorized

The U.S. stock market is walking a tightrope, balancing on the edge of uncertainty. While indices remain elevated, warning signals are flashing red across the board. Overvaluation concerns, slowing earnings, inflationary pressures, and escalating trade tensions are brewing a perfect storm. Will this turbulence lead to a mere market correction, or are we staring at the early signs of a full-blown downturn?

Overvaluation Concerns: Buffett Indicator & CAPE Ratio:

The Buffett Indicator, measuring total market capitalization relative to GDP, currently stands at 192.7%, signalling extreme overvaluation. Historically, such levels have resulted in meagre annual returns of just 0.7%, including dividends.

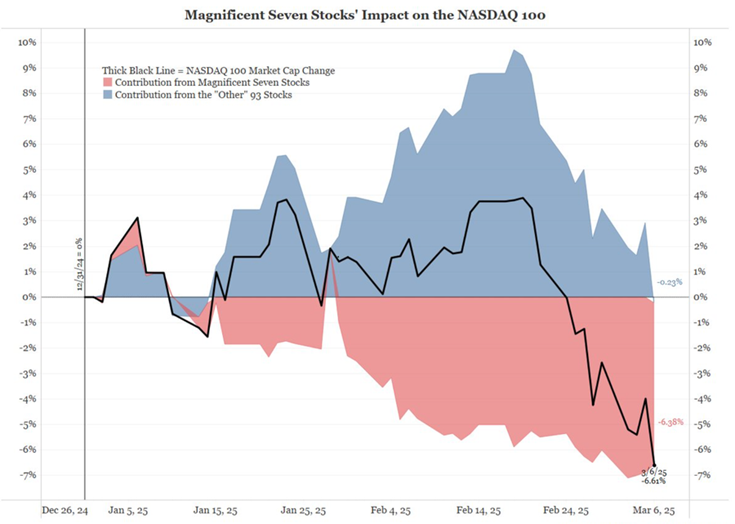

At the same time, the Nasdaq 100 is showing signs of strain, with the Magnificent Seven (Mag-7) no longer propping up the index. As their contribution fades, the broader market is turning negative, pulling the index down. Valuations remain high, with a PE ratio of 33.59 and a CAPE ratio of 41.94, suggesting that earnings growth needs to accelerate significantly to justify current prices.

Mag-7: The Market’s Crumbling Backbone?

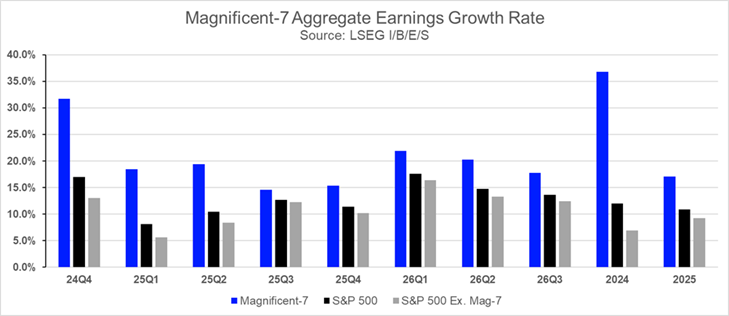

Mag-7 earnings are projected to rise 17.1% in 2025, down from 36.8% in 2024. In the S&P 500, Mag-7 stocks contributed 52% of total net earnings growth in 2024, but this is expected to fall to 33% in 2025. The forward price-to-earnings (PE) ratio for the group stood at 28.3 as of February 28, compared to 21.8 for the S&P 500 and 19.7 when excluding Mag-7.

Despite posting a record $131.2 billion in Q4 earnings (+31.7% YoY), Mag-7 saw its slowest growth since Q1 2023, with Q1 2025 forecasts at 18.5%, indicating a further slowdown. With Mag-7 growth expected to remain subdued, these stocks could face further corrections, dragging down the overall U.S. equity market.

Trade Wars Reloaded: A Market Landmine?

Newly imposed tariffs are adding significant risks to market stability:

- 20% tariffs on Chinese imports, raising costs for electronics and clothing.

- 25% tariffs on imports from Mexico, Canada, and the EU, impacting food, automobiles, and industrial materials.

- Higher steel (25%) and aluminium (25%) tariffs, increasing production costs across key industries.

- 25% tariffs on imported vehicles and auto parts, affecting $286.2 billion in trade.

Retaliatory measures from trade partners, including Canada’s C$30 billion in tariffs and China’s 10%-15% new duties on U.S. imports, threaten to disrupt supply chains and corporate profitability, exacerbating risks to economic growth.

Trade Wars Reloaded: Will History Repeat Trump’s 2018-2019 Tariff Fallout?

March 2018: US Manufacturing PMI was 59.2, reflecting strong expansion when Trump imposed tariffs on steel (25%) and aluminium (10%). Initially, businesses stockpiled supplies, keeping production high.

December 2019: PMI fell to 47.7, signalling contraction as rising costs, supply chain disruptions, and retaliatory tariffs reduced business confidence and demand, weakening the manufacturing sector.

Federal Workforce Restructuring: Labor Market and Government Efficiency Concerns:

The labour market is showing signs of strain due to federal workforce restructuring:

- 75,000 federal employees have accepted buyouts, accelerating mass layoffs.

- US Unemployment rate further ticked upside to 4.1%.

- Job openings have declined to 7.134 million, their lowest level since early 2021.

Consumer confidence is also weakening, with the Conference Board’s Consumer Confidence Index dropping 7.0 points to 98.3, marking its steepest decline since 2021. This is translating into weaker consumer spending, as real personal spending contracted -0.5% in January, posing risks to corporate revenues and overall market stability.

Recession Fears Intensify: Will the Economy Crack?

Economic growth projections are in freefall. The Atlanta Fed’s Q1 2025 GDP forecast nosedived from +3.9% to -2.4% in just four weeks, suggesting that recessionary pressures are intensifying.

Meanwhile, inflation expectations are surging. Short-term inflation is now pegged at 6.0% over the next 12 months, the highest since May 2023. Long-term expectations have also risen to 3.5%—a 30-year high, embedding inflation fears into consumer sentiment. The domino effect is already visible:

- Business confidence plummeted from 53.9 in November 2024 to 27.8 in February 2025.

- The S&P U.S. Equity Risk Premium fell from 103.65 to 95.37, signalling investors’ fading risk appetite.

Technical outlook:

On the technical front, from the current levels of 5614 in S&P 500, it might bounce back towards 6000 or 6100 levels, but the broader view of 5200 remains intact. Once that is broken, it can further move lower towards 4950 levels.

Conclusion: A Market at a Crossroads:

With economic storm clouds gathering, the U.S. equity market faces a period of heightened uncertainty. Overvaluation risks, slowing earnings, inflation pressures, and trade headwinds all suggest that the market’s current stability may be short-lived. Whether this turbulence leads to a full-blown downturn, or a mere correction will depend on corporate earnings resilience, policy responses, and whether history once again repeats itself.

Amit Pabari is a managing director ar CR Forex Pvt Ltd. The views expressed in this article are his personal views.

Source: https://shorturl.at/LgbP9