- April 6, 2021

- Posted by: Amit Pabari

- Category: Economy

The Reserve bank of India in its first bi-monthly monetary policy in the financial year 2021-22 is expected to keep interest rates (repo rate) on hold at 4 percent on April 7, 2021. The probability of the “Rate Unchanged” has significantly increased since the last monetary policy on Feb 5, 2021. The notable point here is India’s COVID cases.

On Feb 5, 2021, the RBI in its monetary policy had kept interest rates unchanged but under the Cash Reserve Ratio normalization process, CRR is hiked by 50 bps to 3.5 percent effective March 27 and 4 percent from May 22 this year. At that time COVID cases in India were around the bottom of 10000/day.

While, exactly two months after that bottom, currently cases are nearly All-Time-High of more than 1,00,000/day. The rise in COVID cases (on the entrance of new variant) with normal vaccine rollout will pressurize RBI to maintain the status quo on policy rates and maintain an accommodative policy stance.

The rate hike factors are likely to be dominated by domestic factors. Each factor is explained as below:

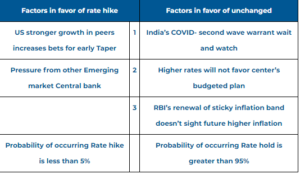

Factors in favor of rate hike

US stronger growth in peers increases bets for early Taper

The risk-on sentiment led by Joe Biden’s “once in a century” infrastructure plan of $2 trillion could attract investment flows back to different US sectors and could help to push growth higher. This has started discounting into future fed’s activity, justifying from recent spike in the US benchmark bond yield. The 2013- taper followed by slow rate hike statement fell short to the market as traders were moving ahead of the Fed for more rate hike. The same is happening right now, Fed is lagging the participant’s foresight for taper & rate hike. The spike in yield on rising inflation and rate hike expectation will pressurize on RBI to turn hawkish.

Pressure from other Emerging market Central bank

The Rupee was an outlier with stronger performance in its peer group on stable economic outlook , rising carry trade and controllable inflation forecast. But recent spike in COVID, shoot up in raw material import prices, higher freight & transport cost, unavailability of container on ports is forcing to recalibrate pricing methodology and wholesale price index is coming in limelight rather than consumer price index. The fall in EM currency on back of rising inflation expectation is triggering central banks to turn hawkish sooner than later.

Factors in favor of unchanged

India’s COVID- second wave warrant wait and watch

The Corona cases with mutant variant, which is less impactful from ongoing vaccine is creating another fear of stricter lockdown in India’s richest city-Mumbai. Overall, Maharashtra is contributing almost 50 percent of corona cases to India’s more than 1 lac cases per day. From growth and financial market point of view, this is not a good sign and market will expect higher liquidity and credit facilities to combat issues of businesses and expenditure. And hence, lower rates will help to survive during this kind of situations.

Higher rates will not favor center’s budgeted plan

The center is planning to borrow INR 12 lac crore in financial year 2021-22 with fiscal deficit target of 9.5 percent of GDP; which is 2.5 times higher than normal levels. This has to be well supported by the central banks. Out of 12 lac crore, borrowing calendar suggests 7.2 lacs worth borrowing (more than 60 percent) will be done by September. And hence, RBI has to keep interest rates at “reasonable” levels to borrow at cheapest levels since 2004-2005. The borrowing calendar suggests issuance is tilted towards long-end to give importance to ‘orderly evolution of yield curve’.

RBI’s renewal of sticky inflation band doesn’t sight future higher inflation

Recently, RBI has supported the government’s inflation target of 4 percent with deviation of +/- 2 percent by renewing flexible inflation targeting regime (FIT) for another five years through 2026, erasing market speculation that government will push to shift focus to economic growth. However, renewal at the steady levels doesn’t seem promising at the current situation and if RBI fails to mitigate inflation target for three consecutive quarters, it has to justify to the government for it. The chances of hitting upper band is more likely on account of rise in crudeoil prices, ignorance of center’s to cut tariff and duty and due to rising food prices. And hence, in this case if underestimating inflation could pressurize on equity market and capital flows. And in extreme case, to curb outflow RBI has to hike rates.

Conclusion:

Overall, the RBI is expected to keep interest rates unchanged with no surprise in stance. But they could come up with new easing financial market measures to cheer up market participants for time being. On communication front, RBI has to clearly address their coordination with the government on borrowing front in the current environment. It is expected that RBI could revise their inflation forecast higher a bit and growth forecast a lower. And in this case, market could start reacting adversely and panic selling could emerge. The impact of selling on domestic currency Rupee will not remain muted and could experience unwinding of carry trade in knee-jerk reaction.

Technically, the recent up move in last two-trading session of the last financial year was notable as USDINR pair jumped from 72.50 to 73.50 levels. The ongoing retracement is likely to remain limited up to 72.90-73.10 zone and expected to resume its up move towards 73.80-74.00 levels in the near term.

-Amit Pabari is managing director of CR Forex Advisors. The views expressed are personal.

Leave a Reply

You must be logged in to post a comment.