- November 23, 2024

- Posted by: Amit Pabari

- Category: Uncategorized

As the U.S. heads into a new political era following the 2024 presidential election, the financial markets are caught in a fierce tug-of-war between two monumental forces: the Federal Reserve’s ongoing rate cuts and Donald Trump’s potentially disruptive economic policies. Despite the uncertainties surrounding Trump’s plans, the Fed’s methodical rate cuts appear to be the stronger contender in this market battle, likely defining economic trends well into 2025 and beyond.

The Fed’s Rate Cuts: The Key to Stability

Following a series of bold rate cuts—including a 50-basis-point reduction and a 25-basis-point cut in November 2024—the Federal Reserve remains committed to securing long-term economic stability. The critical question now is whether the Fed will persist with its aggressive cuts or take a more cautious approach under external pressures, including Trump’s policies.

Several factors point to the likelihood of continued rate cuts:

- Rising National Deficit

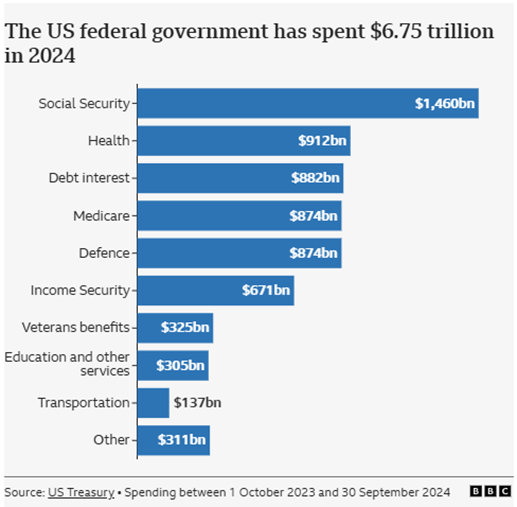

The Federal Reserve’s current revenue stands at $3.27 trillion, while its spending has surged to $6.75 trillion, resulting in a significant deficit of $3.48 trillion. With the prospect of Trump returning to power, there are concerns that government spending will increase further, exacerbating the nation’s growing debt. This situation may necessitate a rate cut by the Fed to manage the fiscal imbalance. Additionally, it is striking that the U.S. government is now spending as much on interest payments as it does on critical sectors like defence, Medicare, and healthcare.

2. Soaring National Debt

The U.S. faces mounting fiscal challenges as national debt surpasses $35 trillion. Debt servicing costs are projected to exceed $1 trillion, prompting the Fed to continue rate cuts to ease borrowing costs. Meanwhile, consumer credit strains are intensifying, with credit card delinquencies hitting 8.8% and serious delinquencies (90+ days overdue) soaring to 11.1% in Q3 2024, the highest since 2011. Credit card debt has reached a record $1.17 trillion, leaving $130 billion at risk of default. These pressures underscore rising financial vulnerability among U.S. households.

3. Bank Losses and Economic Strain

U.S. banks are under immense pressure, with losses on real estate debt securities soaring to $750 billion—seven times the losses seen during the 2008 crisis. Bank of America alone reported a staggering $116 billion in losses over the past three years. The strain on the financial system is palpable. If these challenges continue, the Fed will likely keep cutting rates to stabilize the banking sector, reduce borrowing costs, and prevent a collapse in the real estate market.

4. Falling Household Savings

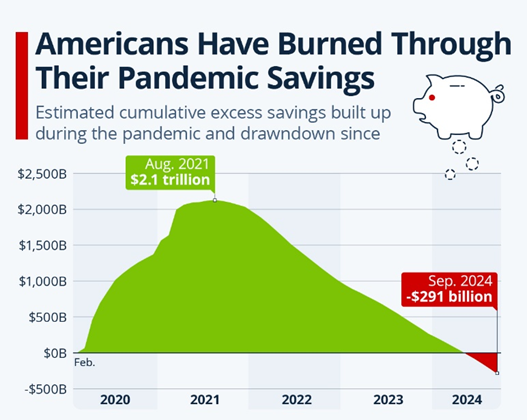

During the pandemic, Americans saved in record amounts, but by September 2024, households were $291 billion short of expected savings levels. This shortfall is creating a drag on consumer spending. To combat this, the Fed will likely use rate cuts to stimulate demand, encouraging both spending and investment to prevent further economic slowdown.

Given these challenges, the Federal Reserve’s rate cuts seem set to continue into 2025. Their goal is clear: to stimulate growth, provide relief to struggling borrowers, and maintain economic stability. Compared to Trump’s economic policies, the Fed’s approach appears more sustainable.

Trump’s Economic Policies: Short-Term Disruption, Long-Term Uncertainty

Trump’s economic policies—marked by aggressive tax cuts and tariffs—could initially create market excitement, but they are unlikely to overshadow the Fed’s rate cuts in the long run. While tax cuts could spur short-term investment and bolster the dollar, they come at a steep cost: a widening fiscal deficit and escalating national debt. This could eventually erode confidence in the dollar, especially as the U.S. grapples with fiscal sustainability challenges. Trump’s trade policies, especially his tariffs on China, may further disrupt global trade relations, potentially triggering inflationary pressures and undermining the dollar’s value. While the Dollar Index (DXY) may stay strong in the short term, its long-term outlook remains uncertain as trade tensions heighten and alternative currencies gain traction.

Moreover, historically, Trump has not been a champion of a strong dollar. During his presidency, the DXY dropped from 101.50 when he took office in 2017 to 88.12 by the end of 2018, and further to 90.58 when he left office in 2021. This suggests his preference for a weaker dollar to stimulate exports. As the Fed continues to cut rates, Trump’s policies could face growing challenges in supporting the dollar in the long term.

Technical Outlook –

On the technical front, the DXY is facing a strong resistance at the 0.5 Fibonacci retracement level around 107.16. A move below this level is expected to push the index toward 103.49. If this support is breached, it could open the door for a decline back to the 100 level.

Fed’s Victory: Shaping the USD/INR and Global Markets

The continued rate cuts by the Fed are beginning to reshape not only the U.S. economy but also global markets, including the USD/INR currency pair. While the dollar remains strong for now, ongoing monetary easing could eventually weaken the greenback, particularly if investors start questioning the sustainability of U.S. fiscal policies.

In India, the outflow of $14 billion from equities in October signals broader concerns about rising interest rates and inflation. However, as the Fed’s rate cuts take effect, there may be renewed interest in Indian equities, especially in sectors like information technology, defence, and clean energy. These sectors, which saw growth during Trump’s first term, could experience a resurgence as investors seek better returns in emerging markets. Despite the potential risks posed by Trump’s trade policies, India’s economic resilience remains strong. With a trade surplus of $54.7 billion in exports versus $28.5 billion in imports, the U.S.-India trade relationship remains a solid foundation. Though tariffs may cause short-term disruption, the strategic partnership between the two nations is likely to continue fuelling growth, particularly in areas of mutual interest.

The USD/INR is expected to remain rangebound, likely trading between 83.80 and 84.50, with a slight bias toward the lower end. The interplay of these factors—Fed policy, Trump’s economic moves, and India’s resilient economy—will influence the currency pair in the coming months. On the global stage, the EUR/USD and GBP/USD are finding robust support at 1.0450 and 1.2550, respectively. These levels are expected to act as springboards for upward movement, with EUR/USD eyeing 1.0800 and potentially reaching 1.10, while GBP/USD targets 1.2850 and possibly 1.3000 in the coming sessions.

Amit Pabari is a managing director ar CR Forex Pvt Ltd. The views expressed in this article are his personal views.

Source: http://surl.li/nqofef