- March 29, 2024

- Posted by: Amit Pabari

- Category: Uncategorized

Gold is a unique asset that embodies characteristics of both commodities and currencies while also serving as an investment asset. Mined like any other commodity, it holds intrinsic value and is sought after during financial uncertainty and geopolitical tensions, making it a form of anti-fiat currency. Its enduring appeal as a store of value spans over millennia. Gold- as a store of value for over 2,500 years has been on a searing 16-month rally, surging more than 30 percent from just above $1,600 per troy ounce in late 2022.

Let’s examine the factors that have been pushing gold prices upward and are expected to persist in doing so…

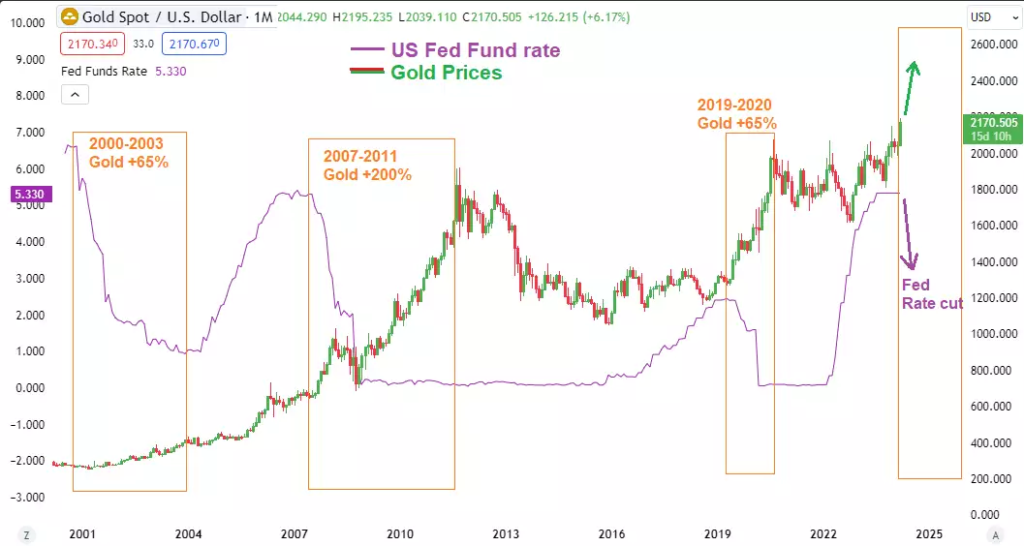

1. Fed on course for a rate cut; lower real yield to support Gold:

The main driving force behind gold prices in the past year has been speculation surrounding the timing of Federal Reserve interest rate cuts. With expectations of the first cut in June, the appeal of holding gold,

which doesn’t generate interest, becomes more enticing as opportunity costs decrease. With a total of four anticipated rate cuts for the year, real interest rates are expected to decline, further increasing the attractiveness of gold as an investment alternative.

Historical analysis of Gold’s performance during the entire rate cut cycle:

Examining the monthly Gold vs US Fed fund rate chart provided, we can observe significant jumps in gold prices during previous rate cut cycles in 2000, 2007, and 2019, with increases of approximately 65%, 200%, and 65%, respectively. With the Fed poised for another potential policy shift in June 2024, gold prices have begun an upward trajectory as traders anticipate higher prices based on historical analysis.

2. Hedge funds’ bullish bets hit a two-year high:

Recent data from COMEX indicates that money managers have initiated new long positions in gold, contributing to its price gains. The increase in open interest suggests that investors are becoming increasingly bullish on gold, rather than merely liquidating existing short positions. The latest data from the Commodity Futures Trading Commission’s disaggregated Commitments of Traders report indicates that money managers raised their speculative gross long positions in Comex gold futures by 28,888 contracts to 173,994 during the week ending March 12. Concurrently, short positions decreased by 2,432 contracts to 32,911.

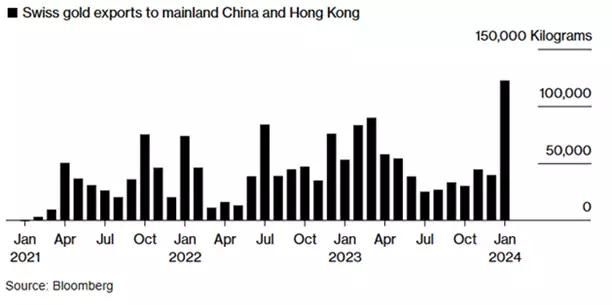

3. Central Banks Embrace Gold Accumulation:

The Russia-Ukraine conflict has been a significant catalyst for central banks to increase their gold reserves. After acquiring 1081.0 tonnes in 2022, they added 1037.40 tonnes in 2023, continuing a trend of 14 consecutive years of buying. The majority of these purchases originated from emerging market central banks, with China (PBOC) leading the pack at 225 tonnes, followed by Poland at 130 tonnes, and India (RBI) acquiring a net 16 tonnes. In January, the Reserve Bank of India (RBI) purchased 8.7 tonnes of gold, marking its largest acquisition since July 2022. This increased the RBI’s gold holdings to 812.3 tonnes in January, up from 803.58 tonnes in December 2023, as reported by the World Gold Council.

This trend is expected to persist in 2024, particularly in light of anticipated rate cuts by major central banks. Central banks’ influence on gold prices remained pivotal throughout 2023, with Swiss exports to China nearly tripling in January as consumers sought a hedge against market turmoil.

4. Endless Uncertainty may support Yellow metal:

Geopolitical tensions, such as Russia’s warnings against US military involvement in Ukraine or the Israel-Hamas conflict, along with the upcoming US election, may further bolster the safe-haven demand for gold. The potential re-election of Donald Trump could amplify safe-

haven demand. Historically, during Trump’s administration, the US implemented various tariffs, potentially sparking another trade war scenario and thereby increasing the appeal of safe-haven assets. According to the table,

following the 2000 election, US gold prices have, on average, surged by 8.74% post-election.

Technical talk on the gold:

After a breakout above $2070, the prices immediately tested $2200; sustaining near $2180 levels. Now, any pullback near $2100-2070 zone will be buying opportunity for the target of $2450-$2500, while one can keep the stoploss of $1975.

Outlook on White Gold- i.e. Silver:

Silver, often dubbed as the “commoner’s gold” for its accessibility, presents an alternative avenue for investment compared to conventional assets, while also serving as a safeguard against inflation through its track record of retaining value over time.

Although silver’s performance in past year may have appeared lackluster in comparison of Yellow metal. Historically, silver has exhibited a tendency to initially lag during bullish periods, a pattern familiar to those in the investment realm. It often begins its ascent quietly, gradually gaining momentum before eventually surpassing gold, as described in the chart. So, believe that Silver should follow the suit and run behind the gold’s bull run path.

Technical talk on the Silver:

As can be seen, Silver prices are on the verge of breaking above $25.90. If so, it will move towards $28.50 to $30.00 over the next 6 to 8 months and if the rally is extended then it will test $35.50 to $40.00.

Outlook on “Doctor Copper”:

The term “Doctor Copper” is refer to copper because of its perceived ability to provide insights into the overall health of the global economy. Copper is often seen as a barometer of economic activity due to its widespread use in various industries, including construction, manufacturing, and electronics.

Despite a sluggish start to the year, China, as the world’s largest consumer of base metals, is expected to ramp up its demand. With China’s announcement of its 5% growth target for 2024 and the implementation of significant reductions in benchmark mortgage rates to support the struggling property market, there are indications of a broader economic recovery.

Supply-side challenges, like power shortages at facilities such as China Nonferrous Metal Mining Corp’s Chambishi Copper Smelter, threaten base metal supply. The smelter, producing 250,000 metric tons annually, slashed one-fifth of its output, affecting Africa’s second-largest copper producer.

Codelco, the world’s leading copper producer, experienced a 16% production drop to 107,000 metric tons year on year, as reported by Cochilco. Overall, we believe that there will be significant upmove in the global copper market.

Technical talk on the Copper:

The weekly chart of Copper indicates a breakout from a symmetrical triangle pattern, followed by a pullback to the Apex point before resuming its upward trend. Looking ahead, there’s an anticipation of a rise towards $4.35 in the short term and $5.05 in the medium term.

In summary, major precious metal and copper prices are showing bullish formations. We anticipate international gold prices to reach $2450-$2500 and silver to hit $29.50-$30.00 in the medium term. Additionally, copper prices could target $4.35 initially, with potential to extend to $5.05. Rising commodity prices typically exert downward pressure on the US dollar due to inflationary concerns, trade deficit widening, reduced economic competitiveness, and a shift in investor preference towards commodity-based assets or currencies of commodity-exporting nations.

Amit Pabari is a managing director ar CR Forex Pvt Ltd. The views expressed in this article are his personal views.

Source: https://shorturl.at/MNSU6